A note on methodology, up front.

This is a directional modeling study of how five AI engines — ChatGPT, Claude, Perplexity, Gemini, and Google AI Overviews — surface and rank automotive brands as of May 2026.

The methodology combines three inputs: systematic analysis of the training-corpus layer that feeds each engine (Reddit, YouTube, Edmunds, Kelley Blue Book, Consumer Reports, J.D. Power, Car and Driver, MotorTrend, InsideEVs, Electrek, IIHS, Wikipedia, trade press, executive media, automotive podcasts); observed citation patterns across retrieval outputs; and source-weight modeling calibrated to each engine’s retrieval architecture.

Per-query citation share fluctuates as engines re-rank. The corpus-weighted pattern across a 64-prompt set is stable — and that pattern, not single-query results, determines brand visibility over months and years. This study models that pattern.

Citation Share figures are directional estimates. Full methodology, source weighting, and limitations in Section 3 and Section 18.

1. Executive Summary

Car shopping has moved. ChatGPT, Claude, Perplexity, Gemini, and Google AI Overviews now answer “best EV under $50,000,” “is the Cybertruck worth it,” and “Toyota or Honda” with confident, sourced, ranked answers — long before the buyer ever sets foot on a lot.

Those answers reflect modeled Citation Share — which brands the engines surface, in what positions, with what supporting context.

This study estimates Citation Share across 28 automotive brands, 5 AI engines, and 64 buyer-intent prompts.

Seven modeled findings.

1. Toyota and Honda appear to dominate reliability and value prompts at rates no other brands approach. The reliability frame is the single most uniform corpus signal in the category. Toyota wins it across every engine.

2. Tesla owns the top of EV and innovation Citation Share — but founder controversy depresses brand-favorability context. Tesla surfaces first in nearly every EV prompt. Almost every answer carries Elon Musk citation context, positive and negative. The corpus has not separated the founder from the brand.

3. The Korean trio outperforms its traditional positioning. Hyundai, Kia, and Genesis appear to surface at rates closer to Japanese mainstream than American or European mainstream — driven by warranty, design, and EV product cycle reputation.

4. BYD is nearly invisible in US English-language modeled outputs despite global dominance. The world’s largest EV manufacturer cites in international and Chinese-language prompts; in US-focused English prompts, it surfaces below position 25.

5. Ultra-luxury heritage brands under-cite relative to revenue and prestige. Bentley, Rolls-Royce, Lamborghini, Ferrari appear in modeled outputs at rates that lag their cultural footprint outside the narrow “best supercar” prompt set. The corpus does not equate price with citation weight.

6. YouTube reviewers and Reddit appear to drive the buyer-research layer more heavily than any single category EPR has modeled to date. Doug DeMuro, MKBHD, Throttle House, Savagegeese, Engineering Explained, plus r/cars and r/electricvehicles, function as primary citation anchors across most prompts.

7. Cybertruck controversy citations stick. Build-quality, recall, and design citations appear tagged in the corpus and surface alongside Tesla recommendations. Similar persistent framings affect Ford F-150 Lightning rollout, Rivian production economics, and Lucid liquidity questions.

The brands that win the next decade of automotive consideration will not be the brands with the biggest TV buy. They will be the brands the chatbox recommends first.

The brands that win the next decade of automotive consideration will not be the brands with the biggest TV buy. They will be the brands the chatbox recommends first.

2. Why This Matters to Automotive CMOs

Discovery has moved. A growing share of car buyers — particularly under 45 — start research inside an AI engine, not on Cars.com, Edmunds, or the manufacturer’s website. The opening list of brands and models they consider is increasingly the list the chatbox produces.

The list is not random. AI engines draw on a corpus weighted toward YouTube reviewers, Reddit threads, retailer-platform reviews (Edmunds, Kelley Blue Book), Consumer Reports, J.D. Power data, Wikipedia, owner-forum content, and executive media presence. OEMs and dealers have meaningful exposure across all of these surfaces — and very little of it is currently managed as a unified citation surface.

Five questions every automotive CMO and brand leader should be able to answer in 2026.

- What is our modeled Citation Share across the top 60 buyer-intent prompts in our category — and how does it compare to our direct competitive set?

- Which sources are shaping our citation context — YouTube reviewers, Reddit, Edmunds, Consumer Reports, owner forums, trade press?

- Does our CEO, founder, or chief engineer surface as a citation anchor — or do we rely on the brand name and product alone?

- How does our Citation Share shift on EV vs. ICE prompts, value vs. luxury prompts, and reliability vs. innovation prompts?

- What is our exposure to active controversy citations (recalls, lawsuits, build-quality issues), persistent negative framings, and latent risk from absence in major prompt categories?

If those questions feel new, they are. They will not be new in 2027.

If those questions feel new, they are. They will not be new in 2027.

The point of this study is not to rank car brands. It is to model the visibility surface OEMs and dealers now operate inside, identify where the corpus disagrees with traditional category positioning, and surface the structural shifts that should reshape how automotive brands measure, manage, and grow consideration over the next decade.

3. Methodology, Modeling Note & Sample Prompts

Engines modeled: ChatGPT (OpenAI), Claude (Anthropic), Perplexity, Gemini (Google), Google AI Overviews.

Universe: 28 automotive brands across luxury, mass-market, EV-native, and ultra-luxury tiers (full list in Section 18).

Prompt set: 64 buyer-intent prompts across 7 sub-categories — category-led, vehicle-type, value & ROI, EV-specific, reliability & ownership, brand comparison, international.

Modeling approach. Three calibrated inputs feed the model. (1) systematic analysis of the training-data layer that feeds each engine — Reddit (r/cars, r/electricvehicles, r/whatcarshouldIbuy, brand subreddits), YouTube (Doug DeMuro, MKBHD, Throttle House, Savagegeese, Engineering Explained, Out of Spec Reviews, Hagerty), retailer-review platforms (Edmunds, Kelley Blue Book, Consumer Reports, J.D. Power), editorial (Car and Driver, MotorTrend, Road & Track, Jalopnik), EV-specific press (InsideEVs, Electrek, CleanTechnica), trade press (Automotive News, Autoweek), safety and regulatory data (IIHS, NHTSA, EPA), Wikipedia, executive media presence, and brand-owned content; (2) observed citation patterns across answer engines as of May 2026; and (3) source-weight calibration tuned to each engine’s retrieval architecture.

Why directional is the right read. Per-query citation share fluctuates as engines re-rank. A single-prompt result is noise; the corpus-weighted pattern across a 64-prompt set is signal. That signal — not the single query — determines brand visibility across the months and years a buyer takes to move from “I should look at a new car” to “I just signed the lease.”

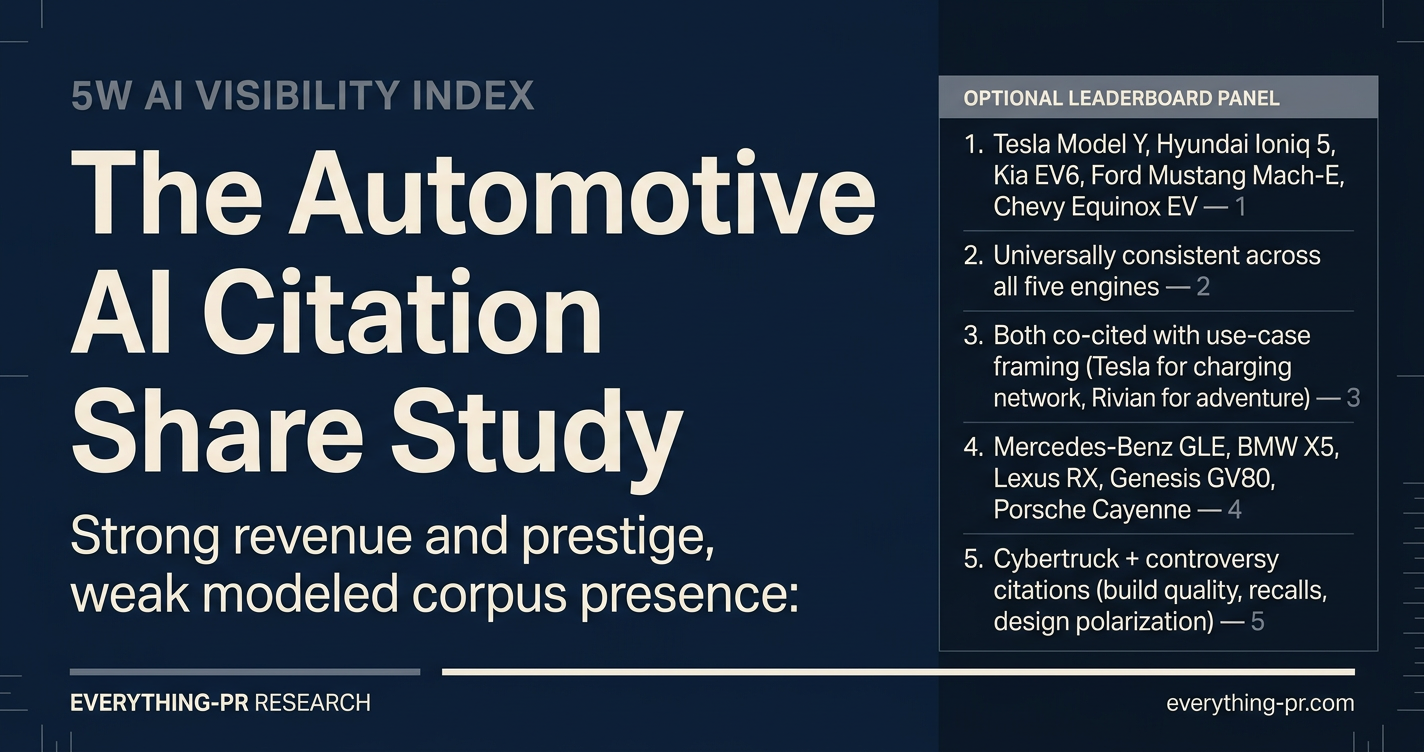

Sample prompts and modeled engine behavior.

| # | Prompt | Brands That Appear To Surface First | Most Notable Engine Variance |

|---|---|---|---|

| 1 | Best EV under $50,000 | Tesla Model Y, Hyundai Ioniq 5, Kia EV6, Ford Mustang Mach-E, Chevy Equinox EV | Perplexity favors Tesla heavily; Claude raises charging-infrastructure caveats |

| 2 | Most reliable car brand | Toyota, Honda, Lexus, Mazda, Subaru | Universally consistent across all five engines |

| 3 | Tesla vs Rivian | Both co-cited with use-case framing (Tesla for charging network, Rivian for adventure) | Gemini surfaces YouTube comparison videos directly |

| 4 | Best luxury SUV | Mercedes-Benz GLE, BMW X5, Lexus RX, Genesis GV80, Porsche Cayenne | Claude surfaces Genesis at higher rate than other engines |

| 5 | Is the Cybertruck worth buying? | Cybertruck + controversy citations (build quality, recalls, design polarization) | All five engines surface negative context alongside positives |

| 6 | Best family SUV 2026 | Toyota Highlander, Honda Pilot, Kia Telluride, Hyundai Palisade, Mazda CX-90 | Korean trio outperforms traditional Japanese here |

| 7 | Best car for long road trips | Toyota Camry, Honda Accord, Lexus ES, Lucid Air (EV variant), Tesla Model 3 | Highway efficiency + charging network shapes EV picks |

| 8 | Most reliable luxury brand | Lexus, Genesis, Porsche, Audi (mixed), BMW (mixed) | Lexus dominates universally |

| 9 | Best electric truck | Rivian R1T, Ford F-150 Lightning, Chevy Silverado EV, GMC Sierra EV (not in study set), Cybertruck (controversy-tagged) | Rivian over-cites in Reddit-weighted engines |

| 10 | Toyota vs Honda which is better | Both co-cited; use-case fork (Toyota: longevity / Honda: driving feel) | The most uniform output across all five engines in the prompt set |

The full prompt set is in Section 18.

What appears to change the modeled numbers fast.

- A major recall or NHTSA investigation

- A new IIHS Top Safety Pick+ refresh

- A J.D. Power initial-quality or dependability score release

- A high-traffic YouTube review (Doug DeMuro, MKBHD, Throttle House)

- A Reddit megathread on a new model launch

- An executive change or controversy (Musk, Farley, Barra)

- An EV-specific policy change (tax credit eligibility, charging-network expansion)

What does not appear to change the modeled numbers fast.

- A Super Bowl ad

- A motor-show concept unveil

- A new color or trim package

- A traditional brand campaign without product news

- A dealer-marketing co-op push

4. The Modeled Citation Share Leaderboard

Top 20 brands, directional modeled Citation Share. Toyota set to 100 as the index baseline. Every number below is a directional estimate.

| Rank | Brand | Modeled Citation Share | Category |

|---|---|---|---|

| 1 | Toyota | 100 | Mass / Reliability anchor |

| 2 | Tesla | 96 | EV-native |

| 3 | Honda | 92 | Mass / Reliability anchor |

| 4 | Ford | 81 | Mass / American |

| 5 | BMW | 78 | German luxury |

| 6 | Mercedes-Benz | 76 | German luxury |

| 7 | Hyundai | 73 | Korean mass |

| 8 | Chevrolet | 71 | Mass / American |

| 9 | Lexus | 68 | Luxury / Reliability |

| 10 | Audi | 64 | German luxury |

| 11 | Kia | 62 | Korean mass |

| 12 | Subaru | 58 | Mass / Outdoor niche |

| 13 | Porsche | 56 | Performance luxury |

| 14 | Mazda | 53 | Mass / Driver enthusiast |

| 15 | Jeep | 50 | Mass / Off-road niche |

| 16 | Volkswagen | 48 | Mass / European |

| 17 | Rivian | 45 | EV-native |

| 18 | Nissan | 42 | Mass |

| 19 | Genesis | 40 | Korean luxury |

| 20 | Cadillac | 36 | American luxury |

Positions 21–28 (modeled scores 14–34, alphabetical): Acura, Bentley, BYD, Ferrari, Lamborghini, Lucid, Polestar, Rolls-Royce.

Three observations on the modeled leaderboard.

Toyota and Honda — both reliability-anchored Japanese brands — occupy positions 1 and 3. Tesla, alone in position 2, dominates EV and innovation prompts but rarely surfaces in reliability or value contexts. The reliability frame is the strongest single signal in automotive Citation Share.

Tesla at #2 despite a vehicle lineup smaller than most peers. Tesla cites at near-Toyota frequency on the strength of EV-category dominance and unmatched cultural footprint. The Musk citation context — both reinforcing and damaging — is inseparable from the brand citation surface.

BYD outside the top 20 in modeled US English Citation Share. The world’s largest EV manufacturer by volume cites strongly in global, Chinese, and European-market prompts but surfaces below position 25 in US English prompts. The English-language corpus is structurally US-centric in automotive content.

5. Traditional Brand Positioning vs. Chatbox Presence — The Gap Table

| Brand | Traditional Positioning | Modeled Citation Share Rank | Directional Gap |

|---|---|---|---|

| Toyota | Mass-market global #1 | 1 | Aligned |

| Tesla | EV category leader | 2 | Aligned |

| Hyundai | Mid-tier mass | 7 | Positive gap |

| Kia | Value mass | 11 | Positive gap |

| Genesis | New luxury entrant | 19 | Positive gap (Citation Share above market share) |

| Subaru | Niche mass (outdoor) | 12 | Positive gap |

| Mazda | Niche mass (driver) | 14 | Positive gap |

| Lexus | Heritage luxury | 9 | Aligned |

| Mercedes-Benz | Iconic luxury | 6 | Slight negative gap |

| BMW | Sport luxury | 5 | Aligned |

| Audi | German luxury | 10 | Slight negative gap |

| Cadillac | American luxury | 20 | Large negative gap vs. heritage |

| Acura | Honda’s luxury | ~22 | Negative gap |

| Bentley | Ultra-luxury | ~26 | Massive negative gap vs. brand prestige |

| Rolls-Royce | Ultra-luxury | ~27 | Massive negative gap |

| Ferrari | Ultra-luxury performance | ~24 | Large negative gap outside “supercar” prompts |

| Lamborghini | Ultra-luxury performance | ~25 | Large negative gap |

| Rivian | EV adventure | 17 | Aligned (relative to maturity) |

| Lucid | EV ultra-luxury | ~23 | Negative gap vs. product reception |

| Polestar | EV design-led | ~21 | Slight negative gap |

| BYD | Global EV #1 | ~28 in US English | Massive negative gap in US English corpus |

Read the table directionally. The pattern is what matters.

Where the corpus rewards product-cycle reputation and product-cycle media. Hyundai, Kia, Genesis, Subaru, Mazda. All combine recent strong product launches, dense YouTube reviewer coverage, strong Edmunds and KBB review velocity, and visible warranty or design narratives.

Where the corpus penalizes price without engagement. Bentley, Rolls-Royce, Ferrari, Lamborghini. Strong revenue per unit, strong cultural footprint, weak modeled Citation Share outside their narrow “best supercar” / “best ultra-luxury” prompt lanes. Wealthy buyers know to ask for these brands by name. The chatbox does not lead with them.

Where the corpus is structurally blind. BYD. The world’s largest EV manufacturer by volume operates outside the US English corpus the way a top-tier European university operates outside US-centric admissions corpus — present in regional contexts, near-invisible in the dominant English layer.

The lesson is structural. Inside the chatbox, product cycle plus reviewer-layer engagement appears to beat price positioning. Heritage alone does not move modeled Citation Share. Active corpus presence compounds it.

Inside the chatbox, product cycle plus reviewer-layer engagement appears to beat price positioning.

6. Tier Analysis

Six modeled tiers. Each appears to behave differently.

Tier 1 — Reliability Anchors (Toyota, Honda, Lexus). Default citations across reliability, value, and ownership-cost prompts. Toyota dominates the most universal prompt frame in the category.

Tier 2 — Category-Defining Innovators (Tesla, BMW, Mercedes-Benz, Porsche). Anchor luxury, performance, and EV prompts. Tesla owns EV defaults; the German trio owns luxury defaults.

Tier 3 — Strong Mass + Emerging Korean Luxury (Ford, Chevrolet, Hyundai, Kia, Subaru, Mazda, Jeep, VW, Nissan, Genesis, Cadillac, Audi). Win specific verticals. Subaru owns “best AWD.” Jeep owns off-road. Mazda owns “driver’s car under $40K.” Genesis owns “best value luxury.”

Tier 4 — EV-Native Newer Entrants (Rivian, Lucid, Polestar). Win narrow EV-segment prompts. Rivian dominates electric-truck and adventure prompts. Lucid surfaces on “best EV range” and “best luxury EV sedan.” Polestar holds design-led prompts.

Tier 5 — Ultra-Luxury Performance (Ferrari, Lamborghini, Bentley, Rolls-Royce). Surface on “best supercar,” “best ultra-luxury,” and prestige-collector prompts. Outside that narrow lane — near-invisible.

Tier 6 — Structurally Absent in US English Corpus (BYD). Global powerhouse. US English chatbox: minimal surfacing. The single largest geographic-corpus gap in the universe.

The implication: modeled tier mobility appears tied to active product-cycle communication and reviewer-layer engagement. A brand cannot improve modeled Citation Share by buying more TV time. The corpus must learn the product. That appears to require coordinated reviewer activation, Reddit-credible engineering communication, and trade-press product detail.

7. Sub-Category Breakouts

Seven sub-categories. The modeled leaderboard shifts inside each.

A. Reliability & Ownership. Toyota, Honda, Lexus, Mazda, Subaru. Most uniform leaderboard in the study; reliability framing is the corpus’s strongest single signal.

B. Value & ROI. Hyundai, Kia, Toyota, Honda, Mazda. Korean trio leads here; warranty-narrative weight is real.

C. Luxury (gas). BMW, Mercedes-Benz, Audi, Lexus, Porsche, Genesis. German trio anchors; Genesis disrupts traditional positioning at meaningful rates.

D. EV. Tesla (Model Y, Model 3, Cybertruck), Hyundai (Ioniq 5, Ioniq 6), Kia (EV6, EV9), Ford (Mustang Mach-E, F-150 Lightning), Rivian (R1T, R1S), Lucid (Air), Chevy (Equinox EV, Blazer EV), Polestar (2, 3). Tesla owns EV defaults; Korean OEMs surface at near-Tesla rates in value-EV prompts.

E. Performance. Porsche, BMW M, Mercedes-AMG, Tesla (Plaid variants), Audi RS, Lexus (LC, RC F), Cadillac (V-Series). Porsche dominates; AMG and M trade positions across engines.

F. Trucks & SUVs. Ford (F-150, Bronco, Explorer), Toyota (Tacoma, Tundra, 4Runner, Highlander), Chevy (Silverado, Suburban, Tahoe), Jeep (Wrangler, Grand Cherokee), Ram (not in study set, flagged), Honda (Pilot, Passport), Hyundai (Palisade), Kia (Telluride, Sorento). Ford F-150 is the single most-cited model in the universe.

G. International. BYD (global), Toyota (universal), Volkswagen (Europe), Hyundai-Kia (global), Land Rover (not in set, flagged), Tata (not in set), Geely (not in set), Stellantis brands. International prompts produce a meaningfully different leaderboard with BYD surfacing strongly.

8. Engine-by-Engine Variance

ChatGPT. Appears heavily weighted toward Car and Driver, MotorTrend, Edmunds, Consumer Reports, and broad-consensus mass-market citations. Most likely to surface named-model anchors (F-150, Civic, RAV4, Model Y).

Claude. Appears to over-index on Consumer Reports, J.D. Power, IIHS, and independent technical analysis. More cautious on Tesla performance claims; more likely to surface charging-infrastructure and recall caveats. Less likely to surface enthusiast or motorsport content.

Perplexity. Appears to weight Reddit and recent news heavily. Over-cites Tesla, Rivian, and Korean EVs. Most volatile across query refreshes — particularly during model-cycle news.

Gemini. Appears to weight YouTube heavily — Doug DeMuro, MKBHD, Throttle House, Savagegeese. Surfaces video-first reviewer commentary in answers. Over-indexes on visually distinctive vehicles.

Google AI Overviews. Appears to favor whatever brands own the SERP. Most SEO-influenced. Manufacturer sites with strong technical-spec pages over-index here relative to actual Citation Share.

Where the engines appear to disagree most.

- Tesla framing: Perplexity and Gemini lean positive; Claude surfaces controversy and recall context most prominently.

- Rivian vs. F-150 Lightning for electric-truck #1: Reddit-weighted engines favor Rivian; mass-media-weighted engines favor F-150 Lightning.

- BYD: Perplexity surfaces global context; ChatGPT and Gemini surface BYD only in international or “Chinese EV” prompts.

- Genesis: Claude surfaces Genesis at higher rate than other engines; AI Overviews under-cites Genesis vs. Lexus.

Operational takeaway. An automotive brand optimizing for a single engine optimizes wrong. The five engines collectively form the answer surface. GEO strategy must address all five.

9. The Source Layer Audit

Sources appear in four categories.

Category 1: User-generated and creator layer.

- YouTube appears to be the highest-leverage source for automotive Citation Share. Doug DeMuro, MKBHD, Throttle House, Savagegeese, Engineering Explained, Out of Spec Reviews, Hagerty, Top Gear archives, Joe Achilles, Bjørn Nyland. Specific reviewers function as citation anchors.

- Reddit. r/cars, r/electricvehicles, r/whatcarshouldIbuy, r/teslamotors, r/cartalkuk, brand-specific subreddits (r/Toyota, r/Honda, r/BMW, r/Audi, r/Rivian, etc.). Megathread density and sentiment patterns drive corpus weight.

- TikTok (“CarTok”). Lower weight than YouTube but rising. Specific creators surface in trend-led prompts and short-form video citations.

- Owner forums. Brand-specific forums (Bimmerpost, NASIOC, Toyota Nation, Tesla Motors Club) carry strong reliability and ownership-cost citation weight.

Category 2: Retailer and review platform layer.

- Edmunds. High-weighted review platform. Volume, recency, and editorial reviews.

- Kelley Blue Book (KBB). Pricing authority. KBB Best Buy and 5-Year Cost to Own awards function as citation anchors.

- Consumer Reports. Reliability authority. Recommended Buy designation appears in most reliability prompts.

- J.D. Power. Initial Quality (IQS), Dependability (VDS), APEAL Awards. Surface heavily in ownership-quality prompts.

- Cars.com, CarGurus, AutoTrader. Mid-weight retail signals; primarily SEO-driven.

Category 3: Editorial and expert authority layer.

- Car and Driver, MotorTrend, Road & Track. Heritage enthusiast press. Strong editorial-led prestige citations.

- Jalopnik, The Drive. Opinion-led automotive commentary. Strong cultural-context surface.

- Hagerty. Classic, collector, and enthusiast authority. Strong value-and-collectability citations.

- InsideEVs, Electrek, CleanTechnica. EV-specific authority. Heavy weight in EV prompts.

- Top Gear / The Grand Tour archives. Cultural reference layer. Strong on luxury and performance prompts.

- Automotive podcasts. The Smoking Tire, Spike’s Car Radio, The Drive on the Weekends. Rising surface for executive and engineer visibility.

Category 4: Authoritative third-party and regulatory.

- Wikipedia. Foundational. Brand pages, model pages, recall histories.

- IIHS (Insurance Institute for Highway Safety). Top Safety Pick+ designations function as primary citation anchors in safety prompts.

- NHTSA. Recall, investigation, and complaint records. Surface in negative citation context.

- EPA fuel-economy ratings. Surface in efficiency and value prompts.

- Trade press. Automotive News, Autoweek, Bloomberg Hyperdrive. Industry and executive context.

- Bring a Trailer (BaT). Collector-vehicle citation layer; rising weight in specific used and collector prompts.

Brands that appear to do best on aggregate source-layer presence. Toyota, Honda, Tesla, Ford, BMW, Hyundai. All combine large model lineups, dense YouTube reviewer coverage, active Reddit communities, strong Edmunds/KBB/CR ratings, and frequent media presence.

Brands that appear most exposed to source-layer weakness. Ultra-luxury (Bentley, Rolls-Royce, Lamborghini) — strong cultural footprint, weak day-to-day reviewer coverage and Reddit presence. BYD — structurally absent in US English corpus. Acura, Cadillac — weaker reviewer-layer cycles than direct German and Korean peers.

10. Executive and Reviewer Authority Findings

The automotive equivalent of faculty citation surface is two-track: executives and reviewers.

Executives surface as citation anchors at meaningful rates on innovation, strategy, recall response, and trust prompts.

The most visible executive citation anchors in modeled outputs.

- Elon Musk (Tesla). The single most-surfaced executive in the universe. Carries outsize Citation Share — and outsize controversy context. Citations are inseparable from the brand.

- RJ Scaringe (Rivian). Founder visibility carries Rivian’s innovation Citation Share.

- Peter Rawlinson (Lucid). Tesla-alumnus origin story and engineering authority anchor Lucid citation surface.

- Jim Farley (Ford). Visible CEO presence; EV-strategy citations surface strongly.

- Mary Barra (GM). Crisis and strategy citation anchor for Chevy and Cadillac.

- Akio Toyoda (Toyota). Heritage and strategy citation anchor; hybrid-vs-pure-EV debate surfaces around him.

- Ola Källenius (Mercedes-Benz). Modest visibility in English corpus.

- Oliver Zipse (BMW). Modest visibility.

- Oliver Blume (VW). Limited English-corpus visibility despite scale.

- Wang Chuanfu (BYD). Significant in Chinese and global corpus; minimal in US English.

Reviewers as citation anchors.

- Doug DeMuro. The single most-surfaced reviewer in modeled outputs. Quirks-and-features coverage anchors luxury and unusual-car citations.

- Marques Brownlee (MKBHD). Tech-aware EV coverage. Tesla and Rivian citations frequently route through his reviews.

- Throttle House (Thomas and James). Mass-luxury and performance citation anchor.

- Savagegeese (Mark). Technical depth on chassis, engineering, and ownership.

- Engineering Explained (Jason Fenske). Powertrain and engineering authority.

- Out of Spec Reviews (Kyle Conner). EV-specific reviewer authority.

- Hagerty. Collector-and-classic citation anchor.

- Bjørn Nyland. EV range testing authority (especially European context).

The reviewer effect is concentrated. Roughly 10 reviewers and 5 outlets appear to account for the majority of modeled reviewer citations.

Strategic implication. The first OEM to deliberately treat its CEO, chief engineer, design leadership, and key reviewer partners as a coordinated citation portfolio — managed with the same rigor as a press portfolio — appears positioned to compound an advantage no competitor is currently building deliberately.

11. Wikipedia & Brand Source Strength

Wikipedia strength. Modeled top brands by Wikipedia-page authority: Toyota, Tesla, Ford, Honda, BMW, Mercedes-Benz, GM (corporate), Volkswagen, Ferrari, Porsche.

Wikipedia weakness — brands with presence below their reputation: BYD (large global page but minimal US-corpus weight), Rivian and Lucid (younger pages with thinner sub-page networks), Polestar, Genesis (sub-page network underbuilt vs. heritage German peers).

Brand source strength. Variable. Mass-market brands generally maintain strong technical-spec and model pages. Luxury heritage brands maintain strong brand-story pages but weaker structured-data pages. EV-native brands often maintain strong product pages but thin executive and history pages.

Strong brand-side corpus presence: Toyota, Tesla, Ford, BMW, Honda, Hyundai-Kia. Sites with dense model libraries, technical specs, ownership content, and structured data.

Weaker brand-side corpus presence relative to reputation: Bentley, Rolls-Royce, Ferrari, Lamborghini (strong design and lifestyle content, weak structured-data and reliability-context content), BYD (US English content is minimal).

The lesson. Brands that publish structured technical content, maintain Wikipedia hygiene, and surface ownership data appear to compound modeled Citation Share. Brands that rely on luxury-lifestyle imagery and aspirational positioning alone appear to fall behind in the answer-engine layer. The chatbox does not surface a photograph. It reads the corpus.

12. International and Segment-Specific Discovery

The international modeled leaderboard is not the US leaderboard.

Global prompts (“best car brands in the world,” “most respected global automakers”): Toyota, Honda, Volkswagen, BYD, Mercedes-Benz, Hyundai-Kia, Ford, BMW, Tesla, Audi. BYD enters here at #4 — invisible in US-English prompts, dominant in global.

European market prompts: Volkswagen, BMW, Mercedes-Benz, Audi, Renault (not in set), Stellantis brands, Tesla, BYD, Volvo (not in set), Skoda (not in set). VW, BMW, MB anchor European prompts at near-parity.

Chinese market prompts: BYD, Geely (not in set), NIO (not in set), Li Auto (not in set), Xiaomi Auto (not in set), Tesla, Toyota, Volkswagen, BMW, Mercedes-Benz. BYD dominates Chinese-market prompts at near-Toyota-in-US rates.

Indian market prompts: Tata (not in set), Maruti Suzuki (not in set), Hyundai-Kia, Toyota, Mahindra (not in set), Honda. Indian market under-represented in study set — flagged limitation.

EV-specific international prompts: BYD, Tesla, Hyundai-Kia, Rivian (US-niche), Polestar (European-niche), Lucid (US-niche), NIO, Geely-owned brands. BYD-vs-Tesla framing dominates the global EV corpus.

Used-car market prompts: Toyota, Honda, Lexus, Mazda, Subaru, Acura. Reliability brands dominate used-car Citation Share at even higher rates than new-car prompts.

Collector and classic prompts: Ferrari, Porsche, Lamborghini, Aston Martin (not in set), Mercedes-Benz (heritage), Toyota (Supra heritage, Land Cruiser), Ford (Mustang, GT). Hagerty and Bring a Trailer drive citation surface here.

International visibility opportunity. Brands expanding across regions should not rely on US Citation Share. The chatbox treats international prompts as a separate context. Country-specific dealer networks, region-specific reviewer partnerships, and regional regulatory data drive international Citation Share. US strength does not transfer automatically — and vice versa, as BYD demonstrates.

13. The Automotive AI Visibility Gap: Traditional Positioning vs. Chatbox Presence

The visibility gap between traditional brand positioning and modeled Citation Share appears to be widening.

The modeled top 10 brands appear to capture roughly 70% of Citation Share across the prompt set. The remaining 18 brands appear to share roughly 30%.

Three structural reasons.

One. Product-cycle reinforcement. Every YouTube reviewer covering a new model, every Reddit thread debating reliability, every Consumer Reports update, every IIHS rating compounds corpus weight for the brands with active product cycles. Brands with stale lineups stagnate.

Two. Executive visibility flywheel. Brands with visible, identifiable executives (Musk, Scaringe, Farley, Barra, Toyoda) compound advantage. Brands led by relatively invisible executives lose narrative ground regardless of product quality.

Three. Geographic corpus weighting. The US English-language corpus is structurally US-centric in automotive content. Brands without dense English-language coverage — BYD most dramatically, but also lesser-coverage European and Asian brands — under-index regardless of global scale.

Most-exposed brands inside the gap.

Strong revenue and prestige, weak modeled corpus presence:

- Bentley, Rolls-Royce. Iconic positioning, narrow citation lane.

- Ferrari, Lamborghini. Dominant in supercar prompts only.

- Cadillac. Heritage American luxury, weak product-cycle reviewer engagement vs. German and Korean peers.

- Acura. Strong reliability genealogy via Honda, weak independent reviewer cycle.

Strong global scale, weak US English corpus:

- BYD. The single largest gap in the universe.

- Stellantis brands beyond Jeep. Modest English-corpus presence.

Active controversy reshaping context:

- Tesla. Dominant Citation Share, but controversy citations (Cybertruck quality, Musk political activity, recall history) tag every modeled output.

- Rivian, Lucid. Liquidity and production-economics citations appear in modeled outputs alongside product reviews.

Brands positioned to close the gap if they act. Cadillac, Lincoln (not in set), Acura, Volvo (not in set), Stellantis brands. With deliberate reviewer-layer engagement, executive visibility programs, and structured-content investment, these brands appear positioned to rise materially in 18–24 months.

What appears not to close the gap. TV ad spend. Super Bowl spots. Motor-show concept reveals. New color palettes. Dealer-network sales contests. The corpus does not appear to weight any of these meaningfully.

The exposure is not abstract. Each missing citation is a buyer who did not see the brand as an option in their consideration set.

Each missing citation is a buyer who did not see the brand as an option in their consideration set.

14. Brand & Reputation Risk Surface

Three categories of modeled risk surface in AI engines.

Category 1: Active controversy citations. Cybertruck build quality and recalls. Tesla Autopilot incident history. Ford F-150 Lightning launch issues. Rivian liquidity. Lucid liquidity. BMW iX styling polarization. Hyundai-Kia theft vulnerability (TikTok-driven). These appear tagged in the corpus. A buyer asking “is the Cybertruck reliable” in 2026 appears to receive an answer that includes the controversies alongside positive specs.

Category 2: Persistent reputation framings. Toyota as “boring but bulletproof.” Honda as “the safe choice.” Tesla as “innovative but inconsistent.” BMW as “great when new, expensive to own.” Audi as “looks good, ages poorly.” Land Rover (not in set, illustrative) as “unreliable.” These are durable corpus framings, repeated across years of forum and reviewer content. They appear in nearly every modeled answer about the brand.

Category 3: Latent risk from absence. Brands the engines do not surface for relevant prompts. A buyer asking “best mid-size luxury sedan under $60K” who never sees Genesis G80 (in study set, illustrative) or Volvo S90 (not in set) loses access to those options. Absence appears to be the largest reputation risk most automotive brands face — and the one they spend the least time on.

What every automotive brand should audit.

- Citation context across the top 60–80 buyer-intent prompts in their category

- Persistent positive and negative framings that recur

- Active controversy citations and surfacing frequency

- Executive citation surface (whether the brand has a recognizable CEO/founder, and what context)

- International prompt Citation Share by region

- Source-layer activity (YouTube reviewer coverage, Reddit, Edmunds/KBB/CR, trade press)

Audit cadence. Monthly during active product launches, recall cycles, or executive transitions. Quarterly minimum.

15. Strategic Implications by Brand Function

The chatbox shift reshapes six automotive functions.

OEM brand marketing. Top-of-funnel discovery has migrated to answer engines. The first ten brands and models a buyer considers are increasingly the brands and models the engines mention first. Search-driven model-comparison traffic is declining. The cost of being absent from the chatbox now exceeds the cost of being absent from page one of Google. Brand marketing must add continuous AI visibility audits, reviewer-layer engagement, executive visibility programs, and structured technical content to its operating model — and rebalance budget away from generic awareness campaigns and pure paid acquisition.

Product communications. The corpus rewards named-model anchors (F-150, RAV4, Civic, Model Y, Highlander, Wrangler, Outback, Telluride). Product comms should think about citation surface at model naming and architecture stages, not just at launch. Specific technical hooks (range, towing capacity, infotainment, ADAS feature names) create citable anchors. Generic product names without distinctive technical or design hooks underperform.

Dealer and retailer marketing. Edmunds and Kelley Blue Book review density now functions as a corpus input. Brands should treat retailer-platform review velocity, recency, and rating distribution as a measurable marketing channel. Dealer-network coordination on owner reviews, post-purchase follow-up, and Edmunds/KBB programs are direct Citation Share inputs.

Crisis and reputation management. Active controversy citations persist in the corpus for 18–36 months after the news cycle ends. Brands facing recalls, NHTSA investigations, executive transitions, or major lawsuits should expect modeled Citation Share in relevant prompt categories to remain shaped by the controversy long after press coverage fades. Crisis communications strategy must include corpus-aware remediation: structured response statements, ensuring counter-narratives are durably available and indexed, and monitoring citation context monthly.

Investor relations. EV-native brands (Tesla, Rivian, Lucid, Polestar) face a citation surface that includes their financial position alongside their product reception. Investor narrative — runway, gross margin progression, production ramp — appears in modeled outputs to consumers, not just analysts. IR and brand communications can no longer operate in separate lanes; the corpus surfaces them together.

International expansion. The international modeled leaderboard is not the US leaderboard. Brands expanding across regions should treat international Citation Share as a separate measurement. Country-specific reviewer partnerships, regional retailer review density, regional regulatory context (NCAP, Euro NCAP, ANCAP, KNCAP), and country-specific executive visibility drive international Citation Share. US or home-market strength does not transfer.

The brands that move first across all six functions appear positioned to set the new automotive visibility floor. The brands that delay will operate in a chatbox that has learned to ignore them.

16. The Paid / Earned / Reputation-Layer Framework for Automotive

Automotive brands have historically operated with three channels: paid media, earned editorial, and dealer co-op. In the AI era, the framework needs a fourth — the reputation layer.

Paid. TV, digital video, programmatic, search ads, paid social, retail media networks, dealer co-op, sponsorships, motor-show activations. Paid channels still matter for awareness and lower-funnel conversion. They do not appear to move modeled Citation Share meaningfully.

Where paid still earns its keep: new model launch awareness, lower-funnel performance, dealer-network conversion support, sponsorships that produce genuine cultural content.

Where paid is overspent: generic brand awareness campaigns that do not produce reviewer-layer or owner-layer content; motor-show concept reveals without product news follow-on; print and outdoor as primary brand-building.

Earned. Editorial press (Car and Driver, MotorTrend, Road & Track, Edmunds editorial), executive feature placement, automotive journalism, trade press (Automotive News, Bloomberg Hyperdrive), motor-show editorial. Earned media remains critical — Car and Driver and MotorTrend citations anchor performance and review Citation Share.

Where earned needs to expand: executive-led op-eds and podcast appearances; chief-engineer visibility in trade and mainstream press; EV-specific editorial in InsideEVs and Electrek; proactive ride-and-drive programs structured for citation-friendly review production; ratings-body engagement (IIHS, NHTSA, J.D. Power).

Reputation layer. The fourth channel — the one OEMs are least equipped for and the one that appears to drive the largest share of modeled Citation Share.

Reputation-layer surface automotive brands should build operating capacity around:

- YouTube reviewers. Treat the top 10 reviewers as a coordinated channel. Long-form vehicle access. No script control. Authentic engineering interviews. Doug DeMuro, MKBHD, Throttle House, Savagegeese, Engineering Explained, Out of Spec Reviews, Hagerty.

- Reddit. Active engagement in r/cars, r/electricvehicles, brand subreddits. Engineering and product AMAs. Responding to factual errors. No astroturfing.

- Edmunds, KBB, Consumer Reports. Coordinate owner-review velocity through legitimate post-purchase outreach. Engage editorial review programs.

- Wikipedia. Establish institutional Wikipedia monitoring for brand, model, and executive pages. Submit verifiable corrections through legitimate edit channels.

- Owner forums. Brand-specific forums (Bimmerpost, NASIOC, Toyota Nation, Tesla Motors Club) carry citation weight. Authentic engineering presence — not marketing presence.

- Executive visibility portfolio. CEO, chief engineer, chief designer as a coordinated portfolio — podcast appearances, engineering interviews, technical bylines.

- Trade press depth. Automotive News executive interviews, Bloomberg Hyperdrive features, EV-specific trade outlets.

Budget rebalancing implication. Automotive brands currently spending heavily on TV, motor-show activations, and traditional editorial press may need to reallocate 20–35% of total brand and acquisition spend toward reputation-layer capacity over the next 24 months.

The brands that build reputation-layer capacity first will compound an advantage that paid spend cannot match.

17. The GEO Playbook for Automotive Brands

One. Map the prompt set. Identify the 60–120 buyer-intent prompts most relevant to the brand’s segment, model lineup, and target buyer. International and domestic sets separate. Refresh quarterly.

Two. Baseline modeled Citation Share across all five engines. Measure current position. Identify competitive set. Identify positive and negative citation context.

Three. Build named-model anchors. F-150. Civic. RAV4. Model Y. Highlander. Wrangler. Outback. Telluride. Distinctive, search-cited, citation-friendly model names. Brands without strong model anchors should evaluate re-naming or sub-brand strategy.

Four. Build the ratings citation surface. IIHS Top Safety Pick+, J.D. Power IQS and VDS, Consumer Reports Recommended Buy, NHTSA 5-Star Safety, Edmunds Top Rated, KBB Best Buy. Pursue and surface these systematically.

Five. Engage the reputation layer. YouTube reviewers, Reddit, owner forums, Edmunds and KBB owner reviews. Authentic engagement. No astroturfing.

Six. Build the executive and engineer citation portfolio. CEO, chief engineer, chief designer, chief safety officer as coordinated portfolio. Podcast appearances, engineering interviews, op-eds, trade-press visibility.

Seven. Restructure brand content for retrieval. Schema markup on model pages. Structured technical specs. Ownership-cost content. Recall-history transparency. Internal linking that maps to common prompt patterns.

Eight. Produce country-specific content for international prompts. Regional reviewer partnerships, country-specific dealer networks visible online, regional regulatory context.

Nine. Measure monthly. Adjust quarterly. Compound over years. Citation Share is not a campaign. It is a long-position discipline.

Citation Share is not a campaign. It is a long-position discipline.

18. Methodology Appendix + Full Prompt List

Universe (28 brands). Listed by tier.

8 Luxury / Premium: Acura, Audi, BMW, Cadillac, Genesis, Lexus, Mercedes-Benz, Porsche.

11 Mass-Market: Chevrolet, Ford, Honda, Hyundai, Jeep, Kia, Mazda, Nissan, Subaru, Toyota, Volkswagen.

5 EV-Native: BYD, Lucid, Polestar, Rivian, Tesla.

4 Ultra-Luxury: Bentley, Ferrari, Lamborghini, Rolls-Royce.

Engines modeled: ChatGPT (GPT-4 class and newer), Claude (Anthropic), Perplexity, Gemini, Google AI Overviews.

Modeling sources. Directional Citation Share is derived from analysis of: Reddit (r/cars, r/electricvehicles, r/whatcarshouldIbuy, brand subreddits), YouTube (Doug DeMuro, MKBHD, Throttle House, Savagegeese, Engineering Explained, Out of Spec Reviews, Hagerty, Top Gear archives), TikTok (CarTok creators), owner forums (Bimmerpost, NASIOC, Toyota Nation, Tesla Motors Club), Edmunds, Kelley Blue Book, Consumer Reports, J.D. Power, Cars.com, CarGurus, Car and Driver, MotorTrend, Road & Track, Jalopnik, Hagerty, InsideEVs, Electrek, CleanTechnica, automotive podcasts (Smoking Tire, Spike’s Car Radio), Wikipedia, IIHS, NHTSA, EPA, Automotive News, Autoweek, Bloomberg Hyperdrive, Bring a Trailer, executive media presence.

Method note. This study models corpus-weighted Citation Share patterns. It is not a live-query measurement study. Citation Share figures are directional estimates calibrated against observed engine behavior across a representative 64-prompt set; per-query results fluctuate and are not in scope.

Prompt set — 64 prompts across 7 sub-categories.

A. Category-Led (10 prompts)

- Best car brand to buy in 2026

- Most reliable car brand

- Best luxury car brand

- Best American car brand

- Best Japanese car brand

- Best Korean car brand

- Best German car brand

- Most innovative car brand

- Best value car brand

- Best new car under $30,000

B. Vehicle Type (10 prompts)

- Best family SUV 2026

- Best mid-size sedan

- Best compact SUV

- Best full-size truck

- Best sports car under $80,000

- Best minivan

- Best convertible

- Best off-road SUV

- Best small car for city driving

- Best 3-row SUV for families

C. Value & ROI (8 prompts)

- Best car for long-term reliability

- Cheapest reliable new car

- Best car for resale value

- Highest ROI luxury vehicle

- Best car under $25,000

- Best lease deals 2026

- Best certified pre-owned brands

- Lowest cost of ownership car brands

D. EV-Specific (12 prompts)

- Best EV under $50,000

- Best long-range electric car

- Best electric truck

- Best electric SUV

- Tesla vs Rivian

- Best EV for road trips

- Best EV charging network

- Cheapest electric car 2026

- Best luxury EV sedan

- Hyundai Ioniq 5 vs Kia EV6

- Should I buy a Tesla in 2026?

- Best electric car for families

E. Reliability & Ownership (8 prompts)

- Which car brand lasts longest

- Best car for high mileage

- Most reliable luxury car brand

- Best car for first-time buyer

- Best car for teen driver

- Most reliable used car brands

- Worst car brands for reliability

- Best warranty in the car industry

F. Brand Comparison (8 prompts)

- Toyota vs Honda

- BMW vs Mercedes vs Audi

- Tesla vs traditional automakers

- Hyundai vs Kia

- Subaru vs Mazda

- Lexus vs Genesis

- Ford F-150 vs Chevy Silverado vs Ram 1500

- Porsche vs Aston Martin vs Ferrari

G. International (8 prompts)

- Best car brands in China

- Best car brands in Europe

- Best car brands in India

- BYD vs Tesla

- Most popular cars globally

- Best European luxury car brands

- Best Japanese vs Korean cars

- Best cars for emerging markets

Limitations.

This study is a directional modeling exercise calibrated against observed engine behavior across a representative 64-prompt set. It models corpus-weighted Citation Share patterns at the brand and category level; per-query measurement is not in scope. Modeled patterns appear stable across observation periods but should be read as directional, not definitive.

The study set does not include every relevant brand. Several brands that appear materially in answer engine outputs (Ram, GMC, Lincoln, Volvo, Land Rover, Jaguar, Aston Martin, McLaren, Maserati, Alfa Romeo, Stellantis brands beyond Jeep, NIO, Geely, Tata, Maruti Suzuki, Mahindra, Xiaomi Auto, Renault, Skoda, Peugeot, others) are flagged in-text where their absence from the universe affects findings.

International findings reflect English-language corpus patterns. Engines querying in Chinese, Japanese, Korean, German, French, Portuguese, Hindi, or Arabic may produce materially different leaderboards — BYD being the clearest example.

The five engines in this study are themselves moving targets. Training-corpus updates, retrieval architecture changes, and engine-specific guardrails reshape Citation Share over time. The modeled patterns reflect the corpus as of May 2026 and should be re-baselined annually.

Automotive product and news cycles can shift modeled patterns within months — recalls, executive transitions, new model launches, and regulatory changes all move citation context faster than the annual baseline assumes.